Debt happens to everyone. You're not alone if you’re carrying more debt now than you’d like. And while debt can feel like a slippery slope, it doesn’t have to be a full-on financial trap. The best thing you can do to keep in control is to be honest about the total you owe, devise a proactive plan to pay it off, and stick to it.

Easier said than done? That depends on your relationship with money, the amount of debt and other factors. But, while paying off your debt isn’t necessarily “easy,” a solid strategy you feel good about can certainly make it more straightforward. Here’s how to get started.

Not all debt is created equal

As we look at popular debt repayment strategies, we need to take a second to clarify the kind of “debt” we’re talking about here. Some debt, like student and business loans or a mortgage, is considered “good debt.” These are long-term, life-changing investments that build value and create greater wealth for you in the long run. They’re likely to be much more significant sums that you have a much longer time horizon to pay off.

Though you definitely need to keep paying them off as part of your overall financial plan, here we’re focusing on “bad debt.” This is primarily high-interest consumer debt, like credit cards, auto loans, and payday loans, that charge a ton in interest if you carry a balance and don’t help you accrue equity or value over time.

You want to pay off these types of debt ASAP to avoid interest charges. As with any debt, falling behind on monthly minimum payments can lead to credit score damage, collections or other stressful situations that we definitely want to avoid. Coming up with your debt repayment plan is crucial to staying on top of bad debt and getting it paid down as soon as possible.

Make a list and check it twice

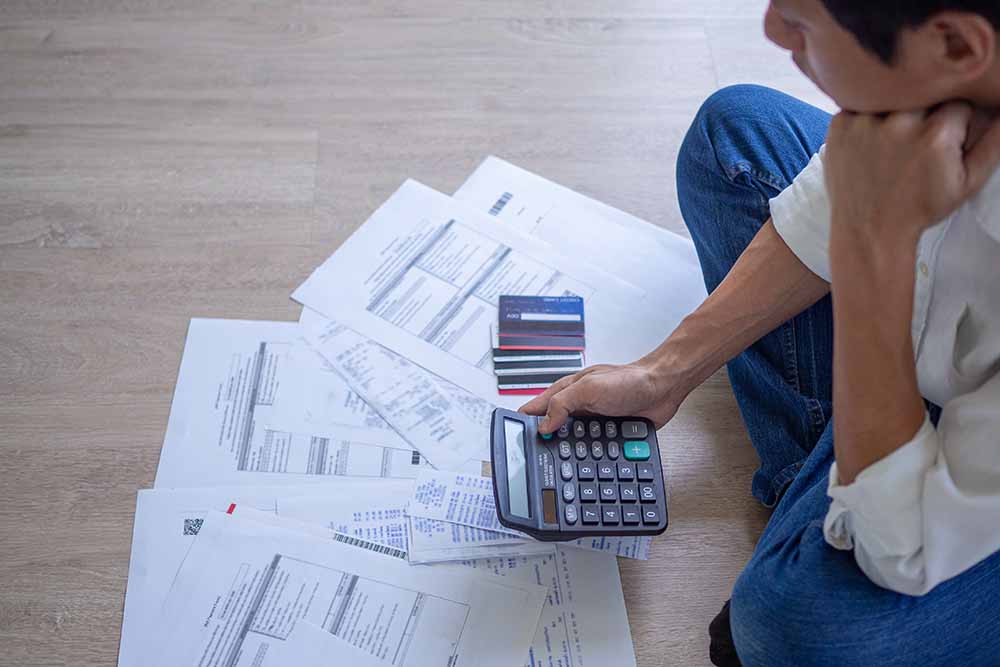

Before you can strategically pay off your debt, you need to know how much debt you have. Financial knowledge is power. It can feel nerve-wracking at first to get a handle on how much total debt you owe — and that’s okay. Take a deep breath and remind yourself that taking control of your finances is positive.

Then sit down and get ready to review your monthly bills and statements. For each account, note the total owed, the minimum monthly payment required, and the interest rate on each bill. Also, check if any accounts are past due and possibly about to be sent to collections. This will all come into play later when you decide which method fits you best to tackle your debt strategically.

Pick your repayment method

Aside from winning the lottery and paying everything off at once (that would be nice!) there’s no one-size-fits-all approach to paying off debt. You’ve got options, and based on your circumstances, choosing the one you’re most comfortable with is your next step to becoming debt-free.

1. The snowball method

Like an ever-growing snowball rolling down a hill, this approach focuses on slowly gathering steam by paying off smaller debts first and then using the newly available funds to pay off larger debts after that.

● Look at your list of all debt totals and pay off the smallest one first. Pay only the minimum on your other debts.

● Once you’ve paid off the first debt, continue to focus on paying off the next smallest debt, and so on.

An upside to the snowball method is that it can give you an immediate boost of confidence and accomplishment, as smaller debts are paid off and help give you a feeling of control.

2. The avalanche method

Another snow-based method (perfect for Canadians!) is just what it sounds like. The opposite of the snowball method, in this approach you start by looking at the highest interest rates or largest amount owed. This will be the largest balance or the one costing you the most in ongoing interest and is adding up by paying it off partially.

● Focus on paying off your largest or highest-interest debt as soon as you can. Pay only the minimum on all your other debts.

● Once your first debt is paid off, use your newly available pay-down funds to move on to the second-largest debt or second-highest interest rate, and so on.

A solid positive to this approach is that it can help you save money owed to interest over the long term. Be aware, though, that based on the size of your debts with this method, it can take longer to pay off, and you need to feel comfortable with that timeline. Once you hit the milestone of paying off a large debt, it’ll be worth it!

3. Consolidation

If you have multiple debts and feel overwhelmed by the different details of paying them off, debt consolidation might be for you. By applying to your financial services provider to consolidate your debt into one payment plan, you can feel some extra peace of mind knowing you’ve only got a single account to pay off. Based on your circumstances, you might also be able to save on the overall interest rate for your consolidation.

This option provides immediate relief and simplicity but leaves you less in control. You need to be fully committed to paying the required payments. Though, if you have a history of letting debt stack up, the extra obligation might help you stick to your plan. It’s key to think about how this type of approach will (or won’t) keep you motivated.

Give yourself a pat on the back and plan for the future

Paying off debt will feel great and give you a fresh start to put your money to work more effectively for you in the future. While some high-interest debt now and then is very common, this is your chance to keep on top of it.

The best way to not have to pay off debt is — surprise — to not incur it in the first place. Once you’ve paid off your debts, look again at your budget, income, shopping habits, and more. Look at the reasons — financial and emotional — why you took on debt, if it was essential, and if there’s a more beneficial approach you could take from now on.

Jeremy Elder is a Toronto-based content marketer and copywriter with over a decade’s experience telling stories for some of the world’s biggest brands. He’s an expert at finding WiFi wherever you least expect it.